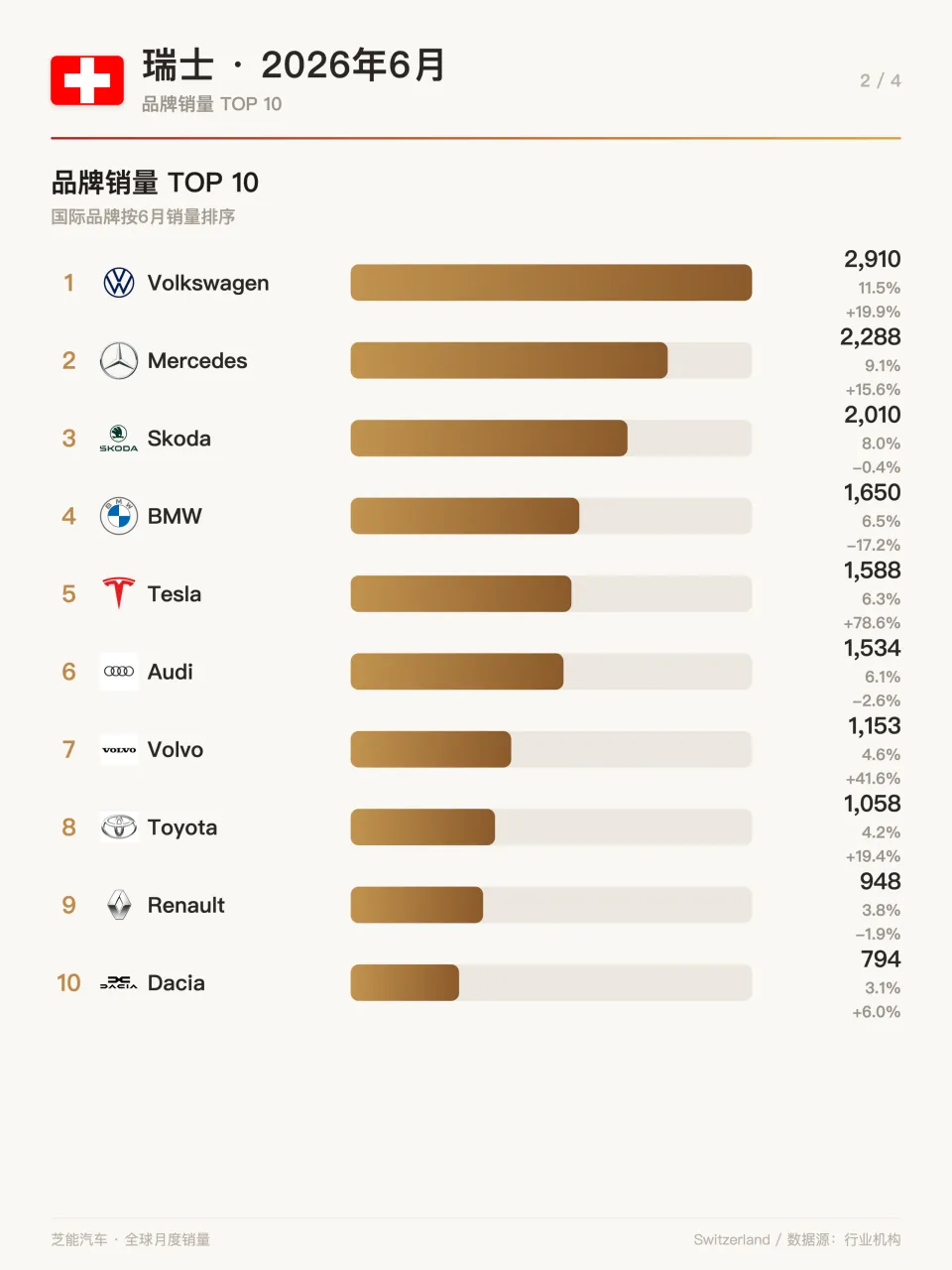

The Jan-Apr 2026 Chinese independent OEM sales top 5 is out: BYD leads with 1.194M units, Chery rises to 2nd with 786K (boosted by exports), Changan 3rd at 732K. Geely and Great Wall round out the top 5 at 621K and 418K respectively. NEV penetration rate has become the decisive ranking variable.

Top 5 Landscape: Sales, Growth, and Structure

The Jan-Apr 2026 top 5 landscape:

| Rank | OEM | Jan-Apr Sales | YoY | NEV Share | Export Share | Avg Price (10K yuan) |

|---|---|---|---|---|---|---|

| 1 | BYD | 1.194M | +18.7% | 100% | 23.9% | 18.5 |

| 2 | Chery | 786K | +42.3% | 28.6% | 51.2% | 12.8 |

| 3 | Changan | 732K | +9.1% | 35.4% | 43.3% | 13.2 |

| 4 | Geely | 621K | +35.6% | 57.7% | 35.4% | 14.6 |

| 5 | Great Wall | 418K | +12.4% | 31.2% | 28.5% | 16.8 |

BYD at 1.194M units firmly holds the top spot, and is the only top-5 OEM with 100% NEV. Its "all-in on NEV" strategy demonstrates powerful scale effects — vertical integration of battery, motor, and control systems gives it 8-12% lower per-vehicle costs than competitors.

Chery at 786K units overtakes Changan for 2nd place, driven by exports. Chery's Jan-Apr exports of 402K units account for 51.2% of total sales, the highest export dependency among the top 5. Tiggo 7, Tiggo 5x, and Omoda perform strongly in Russia, Brazil, South Africa, and the Middle East.

Growth Dynamics: Who Is Burning Future Potential? Who Is Building Momentum?

By growth rate, Chery (+42.3%) and Geely (+35.6%) are the fastest. But the "quality" of growth differs:

Chery: Export growth 68%, domestic growth 18%. High export growth relies on Russia's "window period" (replacement effect after foreign brand exits) and rapid penetration in Brazil, South Africa, and other emerging markets. Risks: Russia's recycling tax hikes, Brazil local factory progress, South Africa currency volatility.

Geely: Domestic growth 28% (Galaxy brand explosion), export growth 245% (April alone at 245%). Domestic growth driven by Galaxy E5, Xingyuan, and Starship 7 EM-i volume; export growth supported by Zeekr, Lynk & Co, and Galaxy differentiated positioning. Risk: Export average prices are rising, but overseas service network density (1,900 outlets) still lags Chery (2,800 outlets).

BYD: 18.7% growth appears to slow, but this is on a high base (1.006M in 2025). More importantly, BYD is shifting from "volume-driven" to "profit-driven" — Q1 2026 financials show per-vehicle net profit rising from 8K yuan in 2025 to 12K yuan, a 50% increase.

NEV Transition: The "Electrification Race" Among Top 5

NEV penetration is the 2026 "watershed":

- BYD: 100% (unmatched)

- Geely: 57.7% (Galaxy + Zeekr dual drive, 80% target for 2027)

- Changan: 35.4% (Avatr + Deepal + Qiyuan three-brand matrix, 50% target for 2027)

- Great Wall: 31.2% (Haval electrification slow, Tank/WEY NEV share rising)

- Chery: 28.6% (Fengyun sequence just started, iCAR brand still incubating)

Geely and Changan are "running" fastest in NEV transition:

- Geely Galaxy brand April sales of 91,001 units, Jan-Apr cumulative 312K, already Geely's largest single brand

- Changan Deepal + Avatr + Qiyuan combined Jan-Apr sales of 187K, accounting for 25.5% of Changan's total

Chery and Great Wall are "half a beat behind" in NEV transition:

- Chery Fengyun sequence (NEV product line) April sales of only 8,234 units, an order of magnitude behind Galaxy's 91,001

- Great Wall Haval brand NEV share of only 18%, Tank 300 Hi4-T and other off-road NEV models slow capacity ramp

Brand Selection Guide for Central Asian and Russian Buyers

For Central Asian and Russian buyers sourcing Chinese independent brands, the Jan-Apr top 5 provides a clear "brand-needs" matching matrix:

- Value for money + mature after-sales: Chery (2,800 global service outlets, Tiggo series #1 in Central Asia market share)

- Technology leadership + charging ecosystem: BYD (Blade Battery + flash-charging network, Uzbekistan/Thailand factories secure supply)

- Intelligence + luxury experience: Geely Zeekr/Lynk & Co (European market validated, rapid premium penetration in Central Asia)

- EREV range freedom + Huawei intelligent driving: Changan Avatr/Deepal (ADS 2.0, EREV variants suited for Central Asian long-distance)

- Off-road capability + rugged style: Great Wall Tank (Hi4-T PHEV off-road, strong adaptability for Russian Far East/Central Asian mountains)

EX1000.COM Q1 2026 export data shows Central Asian and Russian buyer distribution: Chery 31%, BYD 26%, Geely 19%, Changan 14%, Great Wall 10%. This distribution largely aligns with the domestic top-5 ranking, indicating that export market brand awareness is rapidly converging with domestic trends.