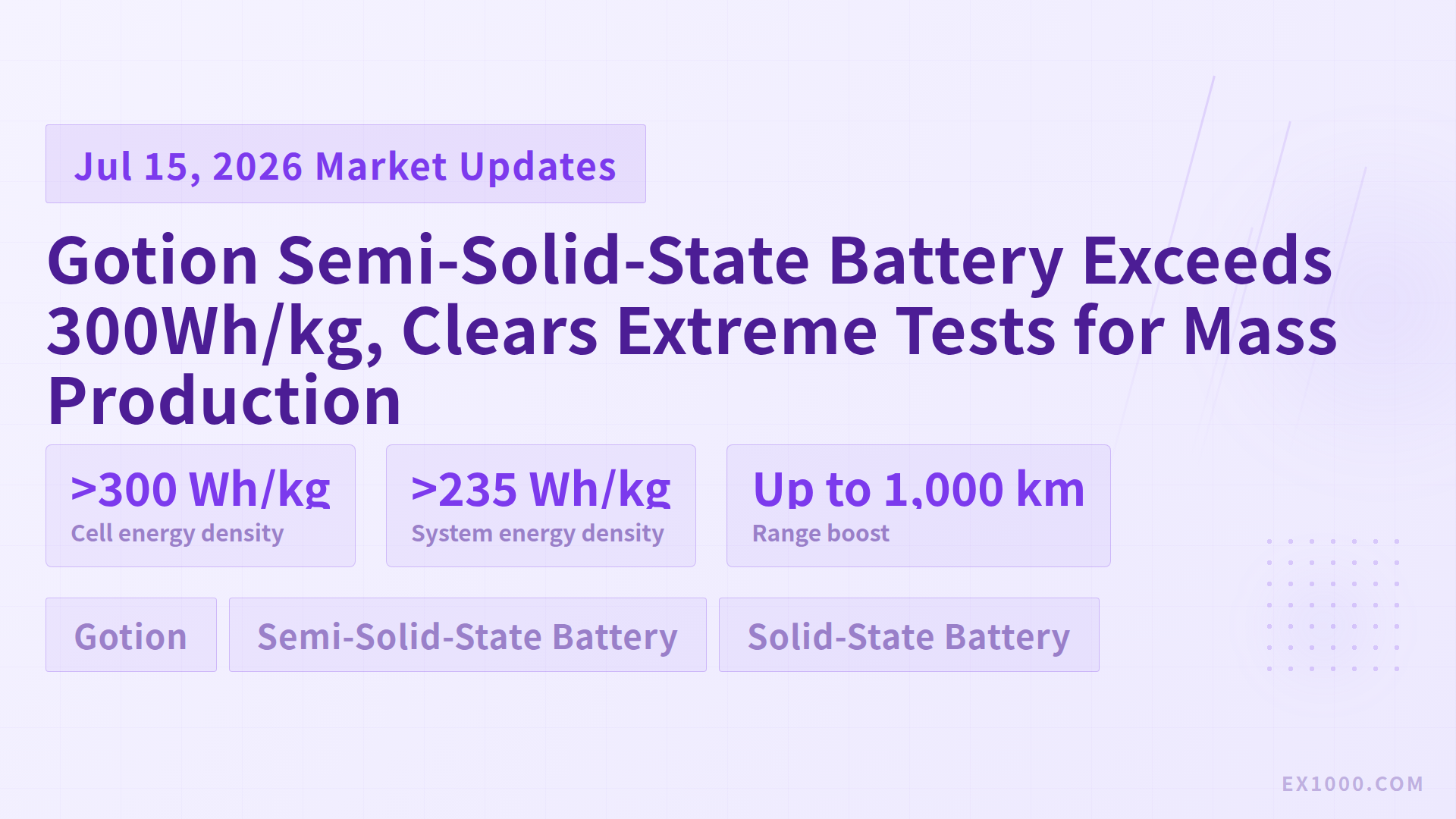

On May 27, 2026, China's MIIT released the solid-state battery standards research guide, outlining a three-phase roadmap from 2026 to 2030: basic research → engineering validation → commercialization. Target energy density: 400Wh/kg (2028) and 500Wh/kg (2030). Semi-solid-state batteries are already in mass production, while all-solid-state batteries are expected to enter small-batch vehicle installation in 2028. Chinese companies hold 65% of global patents.

Policy Framework: Three-Phase Commercialization Roadmap

The MIIT guide establishes the first national-level timeline for solid-state battery industrialization.

Three-Phase Implementation:

- 2026-2027: Basic Research Phase

- Solid electrolyte material screening and optimization

- Interface impedance mechanism research

- Standard testing methodology establishment

- 2028-2029: Engineering Validation Phase

- Small-batch vehicle installation testing

- Manufacturing process feasibility validation

- Safety and reliability certification

- 2030: Commercialization Phase

- Scale mass production

- Cost reduction to commercially viable levels

- All-solid-state battery vehicle launches

| Phase | Timeline | Energy Density Target | Key Tasks |

|---|---|---|---|

| Basic Research | 2026-2027 | 300Wh/kg | Materials, interface mechanisms |

| Engineering Validation | 2028-2029 | 400Wh/kg | Small-batch installation, process validation |

| Commercialization | 2030 | 500Wh/kg | Scale production, cost control |

Technology Status: Semi-Solid in Production, All-Solid Pending

Solid-state battery technology exists on a clear spectrum from liquid to semi-solid to all-solid-state.

Production Progress Comparison

Already in mass production (semi-solid):

- QingTao Energy: 360Wh/kg, supplying IM Motors L6

- WeLion: 320Wh/kg, supplying NIO ET7 (150kWh semi-solid pack)

- Ganfeng Lithium: 300Wh/kg, Phase 1 capacity 2GWh commissioned

All-solid-state development progress:

- Toyota: Sulfide solid electrolyte route, planned 2027 demonstration runs

- Samsung SDI: Oxide route, pilot production starting 2027

- CATL: Condensed battery as transition, all-solid-state small-batch expected 2028

| Technology Route | Representative | Energy Density | Production Status | Expected Installation |

|---|---|---|---|---|

| Semi-solid | QingTao Energy | 360Wh/kg | In production | 2024-2025 |

| Semi-solid | WeLion | 320Wh/kg | In production | 2024-2025 |

| All-solid (sulfide) | Toyota | 400Wh/kg | R&D | 2027-2028 |

| All-solid (oxide) | Samsung SDI | 450Wh/kg | R&D | 2027-2028 |

| All-solid (polymer) | CATL | 500Wh/kg | R&D | 2028-2030 |

Patent Landscape: Chinese Companies Dominate

In global solid-state battery patent competition, Chinese companies hold 65% of patents — an absolute leading position. Regardless of which technical route ultimately prevails, Chinese companies have established first-mover intellectual property advantages.

Patent Distribution:

- Chinese companies: 65%, concentrated on semi-solid and oxide routes

- Japanese companies: 18%, Toyota and Panasonic leading sulfide route

- Korean companies: 10%, Samsung SDI and LG Chem following

- US/EU companies: 7%, mainly startups like QuantumScape and Solid Power

Foreign Brand Acceleration

Toyota, BMW, and Volkswagen are accelerating solid-state battery investments:

- Toyota: Investing approximately 200 billion yen in sulfide all-solid-state development, targeting 2027-2028 installation

- BMW: Partnering with Solid Power, planning all-solid-state models before 2030

- Volkswagen: Investing in QuantumScape, promoting ceramic separator technology

| Company | Technology Route | Investment Scale | Target Installation |

|---|---|---|---|

| Toyota | Sulfide all-solid | 200 billion yen | 2027-2028 |

| BMW | Sulfide all-solid | Solid Power partnership | Before 2030 |

| Volkswagen | Ceramic separator | QuantumScape stake | 2028-2030 |

| CATL | Condensed→all-solid | Internal R&D | 2028 small-batch |

Procurement Implications for Central Asia and Russia Buyers

The technology promise of solid-state batteries is exciting, but the commercialization timeline is clear: mass vehicle installation still requires waiting.

Current Procurement Recommendations:

- 2026-2027 purchases: Semi-solid battery models are already available (IM L6, NIO ET7 long-range), but at premium prices

- 2028+ purchases: All-solid-state models begin small-batch launch, suitable for early adopters

- 2030+ purchases: All-solid-state models achieve scale, costs decline, enter mainstream choice

When sourcing through EX1000.COM, there's no need to delay current needs to "wait for solid-state." Existing ternary lithium and LFP batteries already offer sufficient maturity for daily use and long-distance travel. Solid-state's true value lies in range exceeding 1000km and intrinsic safety improvement, but for most users, current technology is adequate.

Rational Assessment of Technology Maturity

| Battery Type | Energy Density | Production Maturity | Cost Level | Suitable Scenario |

|---|---|---|---|---|

| LFP | 160-180Wh/kg | Extremely high | Low | Urban commuting, cost-sensitive |

| Ternary lithium | 200-250Wh/kg | High | Medium | General use, mainstream choice |

| Semi-solid | 300-360Wh/kg | Medium | High | Premium models, long-range needs |

| All-solid | 400-500Wh/kg | Low | Very high | Gradual普及 post-2028 |

Solid-state batteries represent the industry's future, but they are not a current must-have. For Central Asian and Russian buyers, 2026-2027 procurement decisions should be based on existing technology maturity and cost-effectiveness, rather than paying premiums to wait for immature technology.