The global new energy vehicle charging infrastructure market has surpassed USD 62 billion, with China maintaining its position as the world's largest market with 3.8 million public charging piles. V2G technology, integrated solar-storage-charging systems, and liquid-cooled ultra-fast charging are emerging as new industry trends.

Global Charging Market: Scale Expansion and Divergent Growth Rates

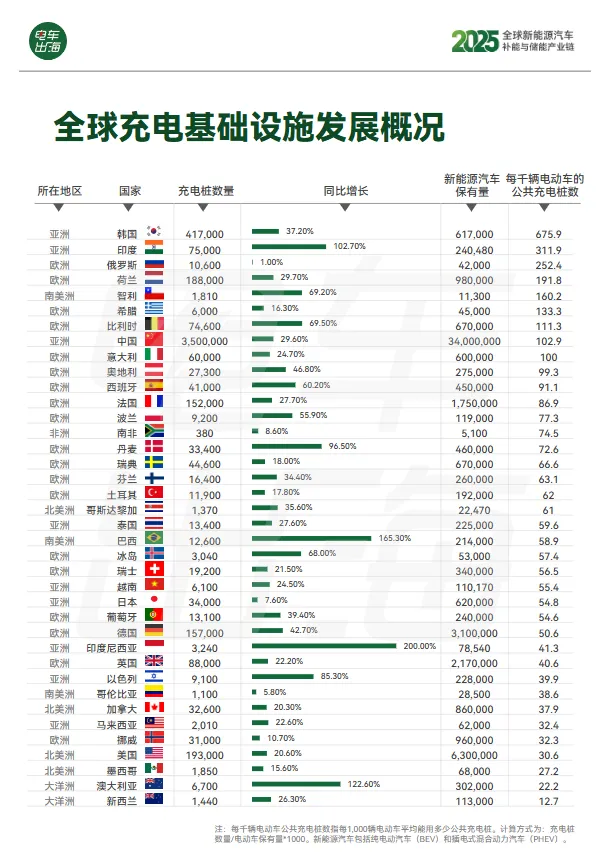

The accelerating adoption of new energy vehicles is forcing global charging infrastructure into a rapid construction cycle. According to the latest industry reports, as of the end of 2025, the global charging infrastructure market exceeded USD 62 billion, up 38.7% from the previous year. Global public charging pile stock reached 8.9 million units, with DC fast-charging share rising to 34.2%, an increase of 6.8 percentage points YoY.

In terms of investment intensity, the industry compound annual growth rate is expected to maintain around 24.5% from 2025 to 2030, with cumulative global charging infrastructure investment exceeding USD 280 billion by 2030. The charging network is transitioning from a "scale expansion" phase to a "quality improvement" phase.

| Region | Public Charging Pile Stock | Global Share | Growth Characteristics |

|---|---|---|---|

| China | 3.8 million | 42.7% | Growth slowing to 19.3% |

| Europe | 2.1 million+ | 23.6% | Driven by carbon regulations, strong growth |

| North America | 580,000 | 6.5% | 67% YoY growth under policy stimulus |

| Others | 2.42 million | 27.2% | Emerging markets gaining momentum |

Regional Divergence: China Leads in Density; Europe Shows Sharp Price Gaps

China continues to maintain its global leadership in charging infrastructure. As of end-2025, China holds 3.8 million public charging piles, firmly the world's largest market, accounting for 42.7% of global total. Charging density exceeds 100 piles per 1,000 NEVs, far above the global average.

In contrast, the European market shows significant charging price divergence. Median charging prices across European countries range from EUR 0.38 to 0.82 per kWh, representing a more than twofold difference. This disparity is driven by varying national electricity market structures, tax policies, operator competition landscapes, and renewable energy penetration rates. For NEV manufacturers planning to export to Europe, charging costs have become a key variable in consumer purchase decisions.

The North American market is accelerating under policy stimulus. Federal funding has enabled the installation of 580,000 public charging piles in 2025, a 67% YoY increase, though overall penetration still lags China and Europe. Emerging markets in Southeast Asia, the Middle East, and Africa are also gaining traction, with Indonesia, Saudi Arabia, and others launching national charging network plans, adding a combined 97,000 new charging piles in 2025.

Technology Evolution: From Fast Charging to V2G and Solar-Storage-Charging Integration

Charging technology iterations are reshaping the refueling experience. In 2026, the industry is showing three clear technological evolution paths:

- High-power liquid-cooled ultra-fast charging: Products with single-gun power exceeding 350kW have achieved mass deployment, with vehicle coverage for charging times under 15 minutes breaking 41%

- V2G (Vehicle-to-Grid): Over 400 communities globally have completed V2G pilot projects, with NEVs charging during grid load valleys and feeding power back during peaks, becoming mobile energy storage units

- Integrated solar-storage-charging: Charging stations are deeply integrating photovoltaic generation with energy storage systems, upgrading from simple "electricity consumers" to "intelligent terminals"

Wireless charging technology has entered commercial validation, with global wireless charging pile shipments reaching 123,000 units in 2025, mainly deployed in autonomous taxi fleets and fixed-route buses. These technology paths not only enhance user experience but also open new revenue streams for charging operators through power ancillary services.

Energy Storage Synergy: The New Growth Pole in the Supply Chain

The boundary between charging and energy storage is blurring. As global NEV stock continues to grow, on-board batteries are becoming the largest distributed energy storage resource. Industry reports indicate:

- V2G commercialization accelerating: The number of charging piles participating in frequency regulation ancillary services reached 187,000, with operators' additional revenue from power ancillary service markets continuing to rise

- Energy storage system coupling with charging stations: Integration of stationary energy storage systems with charging piles effectively mitigates grid peak load pressure and improves charging station operational economics

- China's charging pile exports reached USD 9.87 billion: Up 31% YoY, with primary destinations shifting from Europe to Southeast Asia and South America

For automotive buyers in emerging markets such as Central Asia and Russia, the completeness of charging infrastructure is becoming a critical dimension in evaluating the suitability of NEV models. Charging network density, electricity pricing levels, and charging technology standards directly impact NEV usage costs and user acceptance. For more global charging infrastructure data and procurement analysis, visit EX1000.COM.