China's auto sales reached 15.017 million units in H1 2026, down 4.1% YoY but with a narrowing decline. June NEV sales hit 1.643 million units with 58.5% penetration; domestic brands reached a historic 75.5% share while German brands fell below 10% for the first time.

Core Data: Narrowing Decline and MoM Recovery

On July 9, 2026, the China Association of Automobile Manufacturers (CAAM) released the latest production and sales data, showing that while the H1 market remained in negative territory, warming signs were evident:

- H1 Auto Sales: Cumulative 15.017 million units, down 4.1% YoY, with the decline narrowing compared to the first five months

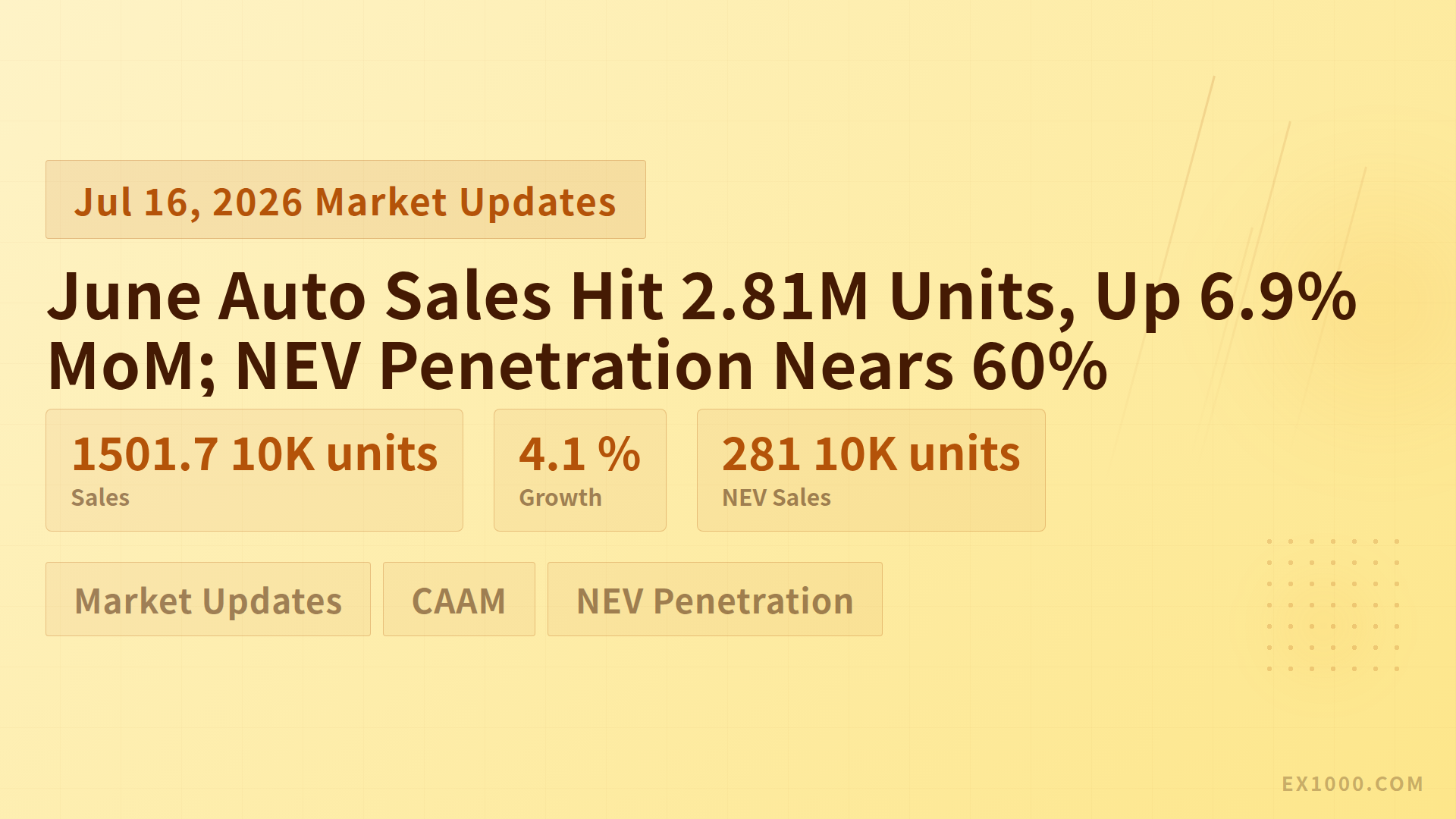

- June Auto Sales: Reached 2.81 million units, up 6.9% MoM

- H1 Passenger Vehicle Sales: Cumulative 12.72 million units, down 6% YoY

These figures send a clear signal: although the overall H1 market has not yet turned positive, the downward momentum is easing. With the continued rollout of NEV rural outreach, vehicle trade-in programs, and local supporting policies, the auto consumption market atmosphere is steadily improving.

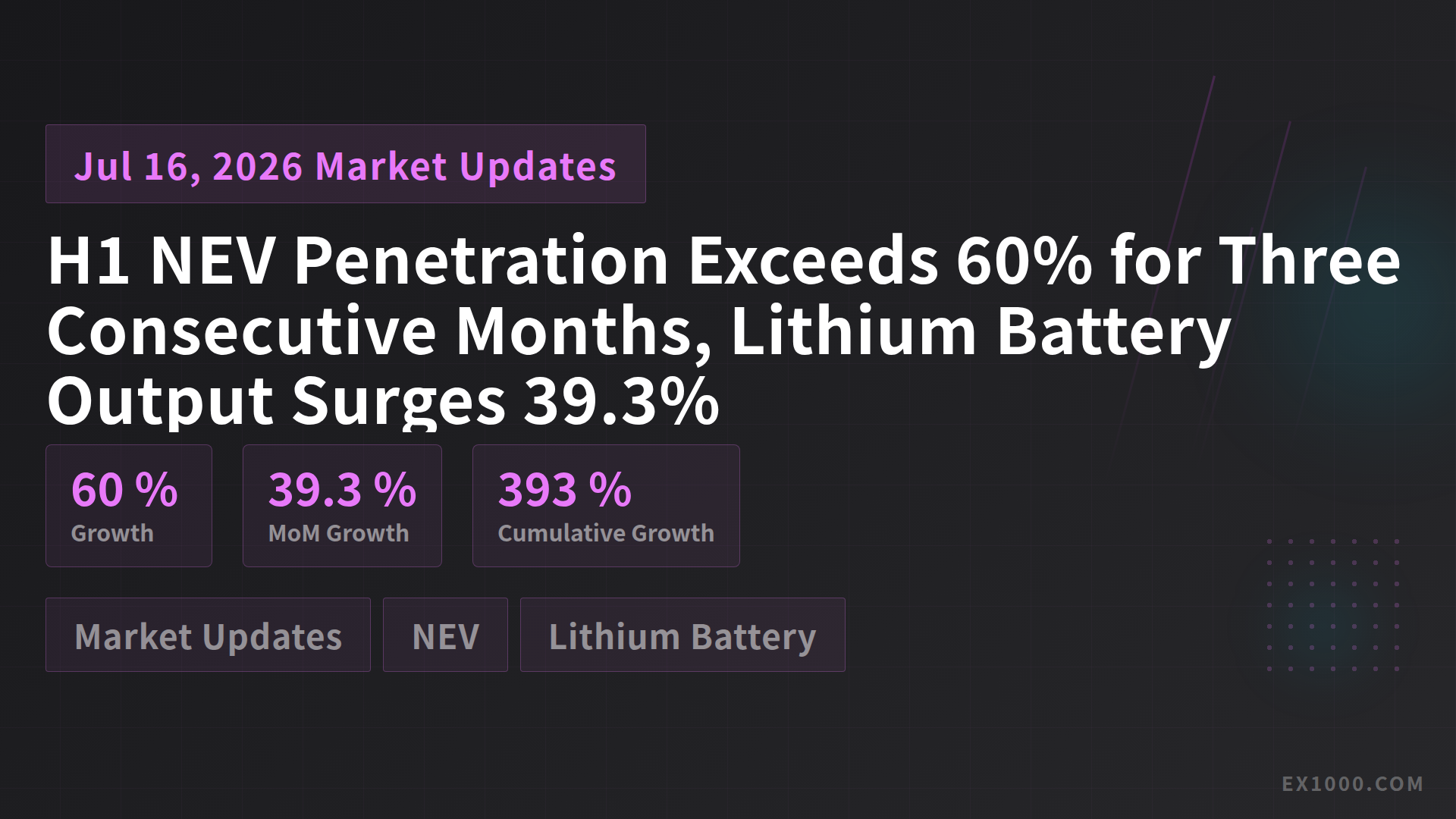

NEV: Approaching the 60% Penetration Milestone

New energy vehicles represent the brightest highlight of the H1 2026 market:

- June NEV Sales: 1.643 million units, up 23.6% YoY

- June Market Share: Reached 58.5%, with monthly penetration nearing the 60% threshold

- H1 NEV Production & Sales: Cumulative 7.446 million units, up 7.3% YoY

- H1 Market Share: Rose to 49.6%

The data shows that the NEV market not only maintained YoY growth exceeding 20% but also saw monthly penetration approaching the 60% psychological barrier. This means that for every 10 vehicles sold, nearly 6 are new energy vehicles. China is becoming one of the world's major auto markets with the highest NEV penetration.

| Metric | H1 Cumulative | YoY Change | June Single Month | MoM/YoY Change |

|---|---|---|---|---|

| Total Auto Sales | 15.017M | -4.1% | 2.81M | +6.9% MoM |

| Passenger Vehicle Sales | 12.72M | -6% | — | — |

| NEV Sales | 7.446M | +7.3% | 1.643M | +23.6% YoY |

| NEV Penetration | 49.6% | — | 58.5% | — |

Brand Landscape: A Historic Breakthrough for Domestic Brands

The June 2026 brand landscape data is particularly striking:

- Domestic Brand PV Market Share: Reached 75.5%, up 8.2 percentage points YoY, breaking historical records for the same period for multiple consecutive months

- German Brand Market Share: Fell to 9.9%, dipping below the 10% threshold for the first time in years

This data set signals a profound restructuring of China's auto market brand landscape. The rise of domestic brands is not driven solely by price advantages but by differentiated competitiveness in intelligent cockpits, assisted driving, and connected vehicle experiences. For buyers in overseas markets such as Central Asia and Russia, Chinese domestic brands' technology iteration speed and feature richness have become core weights in procurement decisions.

Meanwhile, German brands' "break below ten" reflects the continuing pressure on traditional foreign brands in the Chinese market. Against the backdrop of lagging NEV transformation and insufficient intelligent experiences, defending market share has become a common challenge for foreign brands.

Policy Drivers and Future Outlook

The H1 market recovery is driven by a sustained policy push:

- NEV rural outreach: Continuously activating NEV consumption potential in third- and fourth-tier cities and rural areas

- Vehicle trade-in program: Stimulating stock vehicle renewal through subsidies, pulling replacement demand

- Local supporting policies: Measures such as purchase tax incentives, license plate facilitation, and charging subsidies have been rolled out

Looking ahead to H2, with the further strengthening of the trade-in program and the continued enrichment of the NEV product matrix, the market is expected to sustain its recovery momentum. However, it should be noted that the contraction of the traditional ICE vehicle market is still accelerating, and automakers need to make corresponding adjustments in product mix, channel layout, and supply chain management.

For global emerging market auto buyers and dealers, the H1 2026 data from China provides a clear reference: the NEV substitution has entered an irreversible phase, and domestic brands are becoming the biggest beneficiaries of this process. For more market data and procurement analysis, visit EX1000.COM.