CAAM data shows China's auto sales reached 15.017 million units in H1 2026, with NEV market share at 49.6%. Domestic brands surged to 75.5% of the passenger vehicle market, while German brands fell below 10% for the first time.

H1 Sales Data: Positive Signals Amid Decline Narrowing

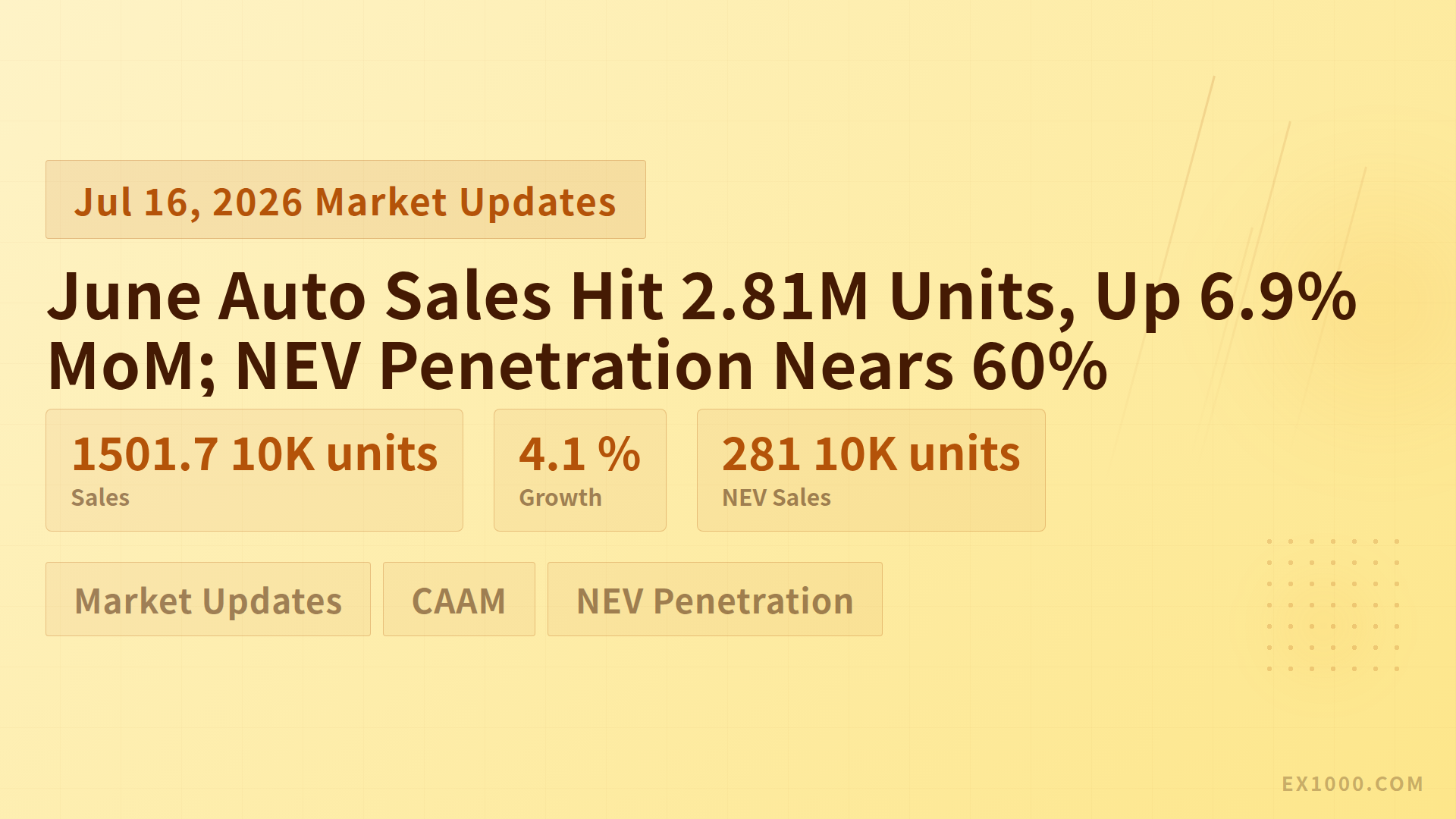

In the first half of 2026, China's auto market exhibited characteristics of "overall pressure with structural optimization." According to the latest data from the China Association of Automobile Manufacturers (CAAM), auto sales from January to June totaled 15.017 million units, down 4.1% year-on-year. However, the decline narrowed compared to the first five months, signaling a warming market trend.

June performance was particularly strong, with auto sales reaching 2.81 million units, up 6.9% month-on-month. For passenger vehicles, H1 cumulative sales were 12.72 million units, down 6% year-on-year.

NEV Market: Penetration Continues to Climb

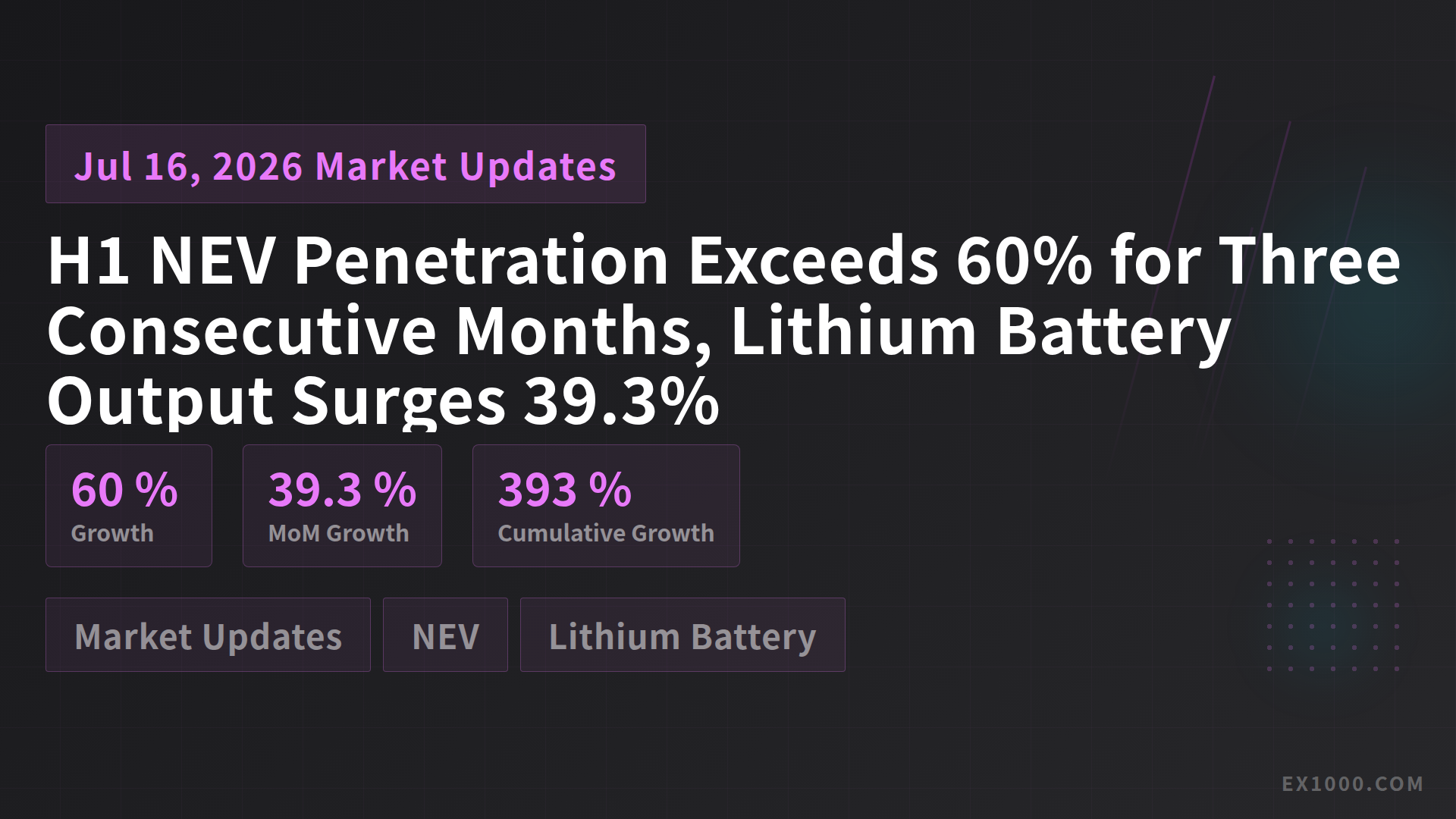

New energy vehicles remained the core engine driving market growth. In June, NEV sales reached 1.643 million units, up 23.6% year-on-year, with a market share of 58.5% — monthly penetration approaching 60%.

For the first half overall, NEV production and sales reached 7.446 million units, up 7.3% year-on-year, with market share rising further to 49.6%. This means one in every two cars sold is a new energy vehicle.

The rapid growth of the NEV market is fueled by sustained policy support:

- New energy vehicle rural promotion campaigns steadily advance, boosting lower-tier market growth

- Vehicle trade-in policies continue to stimulate replacement demand

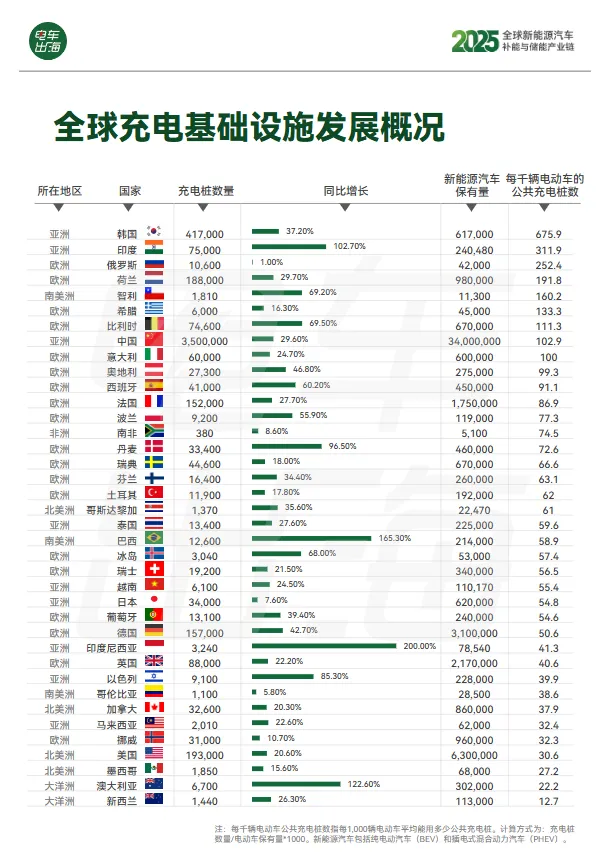

- Local subsidies and charging infrastructure improvements form a policy synergy

Brand Reshaping: Domestic Brands Surge, German Brands Retreat

The competitive landscape is undergoing profound changes. In June, domestic brand passenger vehicle market share reached 75.5%, up 8.2 percentage points year-on-year, breaking historical records for the same period for multiple consecutive months.

In stark contrast, German brand market share fell to 9.9%, dropping below 10% for the first time in years.

| Brand Camp | June Market Share | YoY Change | Trend |

|---|---|---|---|

| Domestic Brands | 75.5% | +8.2pp | Expanding |

| German Brands | 9.9% | Declining | First drop below 10% |

This structural shift reflects three deeper trends:

- Smart cockpits and assisted driving have become critical weights in consumer purchase decisions

- Local brands' advantages in supply chain vertical integration and cost control continue to amplify

- Traditional brand premiums of joint ventures face challenges in the mid-to-high-end NEV market

H2 Outlook

With continued policy dividends and intensive new product launches, China's auto market is expected to maintain its warming trend in H2 2026. For buyers and dealers in overseas markets such as Central Asia and Russia, the selection of export models from Chinese domestic brands will become more diverse, with price competitiveness and intelligent configuration advantages worth noting. For more information, visit EX1000.COM.